What Happens Now That the Fed Cut Interest Rates?

The Federal Reserve has finally cut interest rates, a move that the market had eagerly anticipated for some time. Over the past year, investors consistently speculated that rate cuts would happen sooner and be larger than what ultimately transpired. The Fed reduced the Federal Funds Rate, or the overnight lending rate for the largest financial institutions, by 50 basis points (bps). Along with the rate cut, the Fed released data reflecting its projections for the future path of rates. Once again, the market expects larger and faster cuts than are likely to occur. So, what does this mean for investors and consumers?

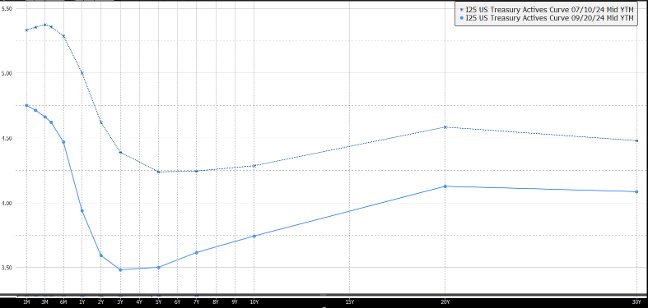

On July 11, 2024, the Bureau of Labor Statistics released its Consumer Price Index (CPI), which surprised many by revealing a more significant slowdown in inflation. Following this, market confidence grew that the Fed would soon cut rates. Investors quickly responded by buying U.S. Treasuries, causing rates to drop sharply. While the Fed controls the overnight rate, market participants drive other rates based on their expectations for Fed actions, the economy, employment, and inflation. The graph below shows the decline in interest rates between July 10 (the day before the CPI release) and September 20. Over this period, the 10-year Treasury yield fell from 4.285% to 3.742%, and the 2-year Treasury yield dropped from 4.621% to 3.593%.

These interest rate movements are where the real impact on investors and consumers can be seen. Assets are repriced at these much lower interest rates, which improves valuations—particularly in interest-rate-sensitive sectors like real estate. For consumers, borrowing costs are also decreasing. According to Bankrate.com, the 30-year U.S. home mortgage rate fell from 7.20% to 6.64% over the same period. As the Fed likely continues to lower rates, shorter-term interest rates should decline further. Longer-term rates may also decrease, but the market has probably already priced in much of this move.

The U.S. economy remains resilient, although there are some signs of weakness in the labor market. Overall, consumers are in relatively good shape, and their debt costs are falling. Equities may become more attractive as money market rates decline along with the Fed’s rate cuts. We remain bullish on both the economy and stock markets.

US Treasury Yield Curve – 7/10/2024 vs 9/20/2024

Source: Bloomberg LP

DISCLOSURE

Innovative Portfolios, LLC (“IP”) is an SEC-registered investment advisor founded in 2015. Clients or prospective clients are directed to IP’s Form ADV Part 2A prior to deciding to participate in any portfolio or making any investment decision. The views and opinions in the preceding publications are subject to change without notice and are as of the date of the report. There is no guarantee that any market forecast set forth in any commentary will be realized. This material represents an assessment of the market environment at a specific point in time, should not be relied upon as investment advice, and is not intended to predict or depict performance of any investment. Any specific recommendations or comparisons that are made as to particular securities or strategies are for illustrative purposes only and are not meant as investment advice for any viewer. The companies mentioned in the publications may be held by Sheaff Brock Investment Advisors, Innovative Portfolios, Innovative Portfolios’ ETFs or any other affiliates or related persons. Therefore, there is a conflict of interest that the advisors may have a vested interest in the Companies and the statements made about them. Past performance does not guarantee or indicate future results.